It’s almost 2026! Unfortunately, the cliff is back.

In 2020, I had a friend who fell off of it. She crashed into an unexpected $10,000 expense. She made slightly more money than she predicted and it pushed her right over the edge. She had to pay back all of the government subsidy money she received the previous year for her insurance premiums.

Insurance rules change regularly. In 2021, the cliff smoothed out to a slope. You only had to payback the difference if you made more money than you anticipated. For example, if you went over by a $1 into the next income bracket you would maybe owe a few hundred dollars back to the government rather than thousands. When it is a cliff, you owe everything back.

Currently, the cliff is set to return in 2026.

That means if you (and your family) make over a certain amount, you will not receive any tax credits for insurance premiums.

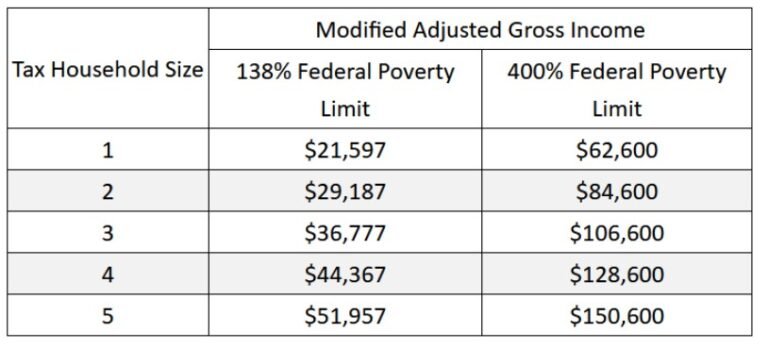

Let’s say for example, you and your spouse expected to earn $84,000. You enrolled in the ACA and received $900/month in subsidies. You unexpectedly earned a $1500 bonus.

You just fell off the cliff.

That bonus money puts you at $85,500 which is over the $84,600 cliff. You now owe $900 x how many months you received the subsidies. If you didn’t realize this until tax time the following year, you could owe 12 months of subsidies. So in this example, you would owe $10,800. That bonus ended up costing you $9,300.

That’s a steep cliff for many of us.

See below for the estimated 2026 income thresholds and don’t fall off the cliff!!

**All numbers are illustrative only and not exacts of incomes or subsides.

**This is a blog. Not financial advice. Make your own decisions. See disclaimers.